Investment Sale

Record this when you sell stocks or ETFs from your brokerage holdings.

What you enter

| Field | Required | Description |

|---|---|---|

| Date | Yes | Settlement date of the trade |

| Symbol | Yes | Ticker symbol of the security |

| Units | Yes | Number of shares sold (all or part of your position) |

| Price per unit or Total amount | Yes | Sale price per share, or total proceeds |

| Fee | No | Trading commission (if not already deducted from total) |

| Superficial loss controls | No | Appear only when you sold at a loss — let you deny part of the loss and defer it (see below) |

What happens

The proceeds split depends on whether you sold at a gain or loss:

At a gain (proceeds > cost base of shares sold):

- The cost base portion is recovered pro-rata: borrowed recovery goes to Borrowed Cash, personal recovery goes to Personal Cash

- The gain (proceeds minus cost base) goes entirely to Personal Cash

- Deductible invested principal decreases by the borrowed recovery; Non-deductible principal increases by the same — this capital is no longer funding an investment

At a loss (proceeds < cost base of shares sold):

- Proceeds are split pro-rata based on the position's borrowed/personal ratio

- The unrecovered borrowed capital stays as deductible invested principal per the CRA's disappearing source rule — the investment is gone, but the debt retains its deductible character

In both cases, the holding's units, cost base, and borrowed cost base decrease proportionally. Recovered borrowed cost goes to Borrowed Cash; recovered personal cost plus any gain goes to Personal Cash.

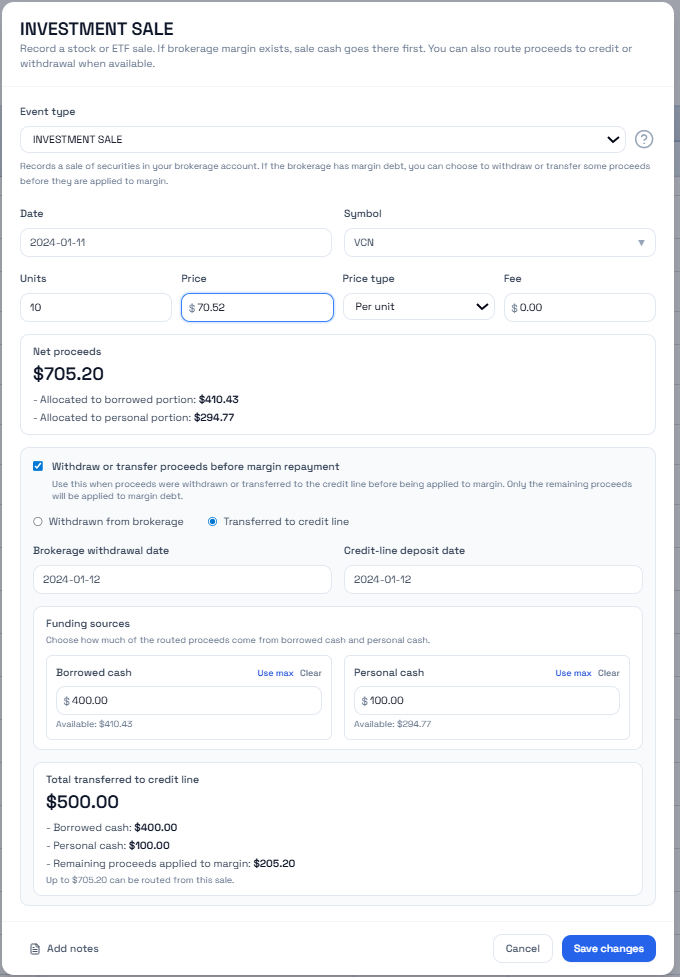

If the brokerage is in margin state, sale proceeds repay margin before becoming brokerage cash. Borrowed capital recovered from a margin-funded investment can directly reduce investment-purpose margin debt. Any remaining proceeds repay the rest of the margin balance based on its deductible/non-deductible composition. Only excess cash after margin is cleared becomes borrowed or personal brokerage cash.

Routing sale proceeds

When margin is enabled and the brokerage is already in margin state, you can route part of the sale proceeds directly to a credit transfer or personal withdrawal when available.

The app handles this as a linked flow: the routed proceeds do not first become ordinary brokerage cash. The event detail explains how much was applied to margin, credit, or withdrawal.

Superficial loss rule

When you sell at a loss and buy the same security back within 30 days before or after the sale — and still hold it at the end of that window — the Canada Revenue Agency's superficial loss rule denies part or all of the loss. The denied loss is not lost: it is deferred by adding it to the cost base (ACB) of the repurchased shares, so it reduces a future gain (or increases a future loss) instead.

When you record a sale at a loss, the app checks for a repurchase of the same security in the window in this account. If it finds one and you still hold units at the end of the window, it shows a warning and suggests a denied amount using the CRA partial-disposition formula. You can apply, edit, or ignore the suggestion.

These controls appear only when the sale is at a loss:

| Control | Description |

|---|---|

| Apply the superficial loss rule | Turns the adjustment on for this sale |

| Denied (disallowed) loss | The portion of the loss you cannot claim this year. Defaults to the suggested amount and cannot exceed the loss on the sale |

| Add the denied loss back to ACB | Check when you repurchased in this tracked account — the denied loss is carried in the holding's cost base and its borrowed/personal split. Leave unchecked when the repurchase was in another account or a registered account (RRSP/TFSA): the loss is then reduced for reporting only and your balances do not change |

Account scope. This check only sees the activity in this account. The CRA applies the rule across all your non-registered accounts and affiliated persons (for example, a spouse), so review your full picture before relying on the suggestion.

The Adjusted Cost Base report shows, per disposition, the capital gain/loss, the superficial loss denied, and the resulting allowable (claimable) gain or loss.

Common questions

How are proceeds split? Based on the position's borrowed/personal cost ratio at time of sale. If 70% of cost was borrowed, 70% of the recoverable amount returns as borrowed cash.

What happens with partial sales? A proportional slice of cost base is removed. The remaining shares keep the same borrowed/personal ratio.

Do I need to record capital gains separately? No. The app calculates gain or loss automatically from proceeds vs. cost base.

What is the superficial loss rule? If you sell at a loss and buy the same security back within 30 days before or after the sale — and still hold it at the end of that window — the CRA denies part or all of the loss. The denied amount is not lost: it is added to the cost base of the repurchased shares and deferred to a future sale.

When should I check "Add the denied loss back to ACB"? Check it when you repurchased the security in this same tracked account, so the deferred loss is carried in the holding's cost base. Leave it unchecked when the repurchase was in another account or a registered account (RRSP/TFSA) — then the loss is reduced for reporting only and your balances do not change.

Learn more

- Selling holdings — how the proceeds split works conceptually

- Brokerage margin — how sale proceeds behave when margin exists

- Brokerage Transfer to Credit — routing proceeds to credit

- CRA rules applied — what happens to deductibility after a sale

- Glossary: Superficial loss rule — quick definition